Every company invests time and resources in understanding their finances. They know exactly where their money is, how they should invest, what costs they should cut on, etc. A good financial plan for freelancers should be part of your strategy too, but it can be an overwhelming task. Because let’s face it, money management and financial planning is not the reason why freelancers decided to start their businesses in the first place!

How much money should I put aside for taxes?

I have these expenses, but the client hasn’t paid me yet…

How much money do I need to start freelancing without worrying?

This piece will help you make better financial decisions as a freelancer.

What is financial planning and why is it key for freelancers?

Financial planning for freelancers is, as the name suggests, the process of planning out how your money, investments and other assets can help you reach your personal and professional goals.

The goal of a financial plan for freelancers is to help you cover costs and mitigate the impacts of unforeseen changes and circumstances.

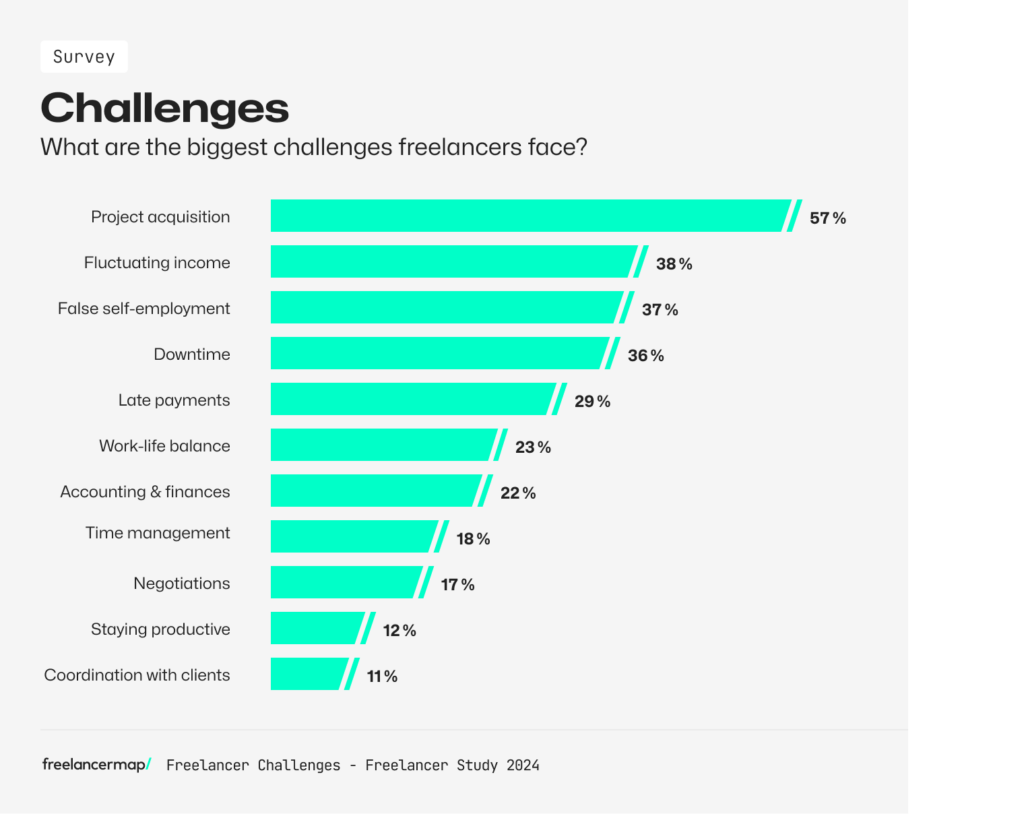

According to freelancermap 2025 study, 38% of freelancers mention fluctuating income as one of the major challenges they face.

While full-time employees have the luxury of receiving benefits from the company they work for, freelancers have to rely on their own financial management to cover costs and make a profit. This is especially overwhelming if you consider how common late payments are in the freelancing world.

This is why a financial plan for freelancers is crucial. Not only does it help you spread your income to cover any unforeseen expenses, it can also improve your financial understanding and help you create an investment portfolio.

Join our freelancer community today!

Create your profile in just 2 minutes and start attracting new clients.

Types of financial reports every freelancer needs

There are a few necessary reports that freelancers need in order to have an efficient financial plan. These can include:

- Profit and loss statements

- Cash flow statements

- Monthly financial reports

- Balance sheets

- Accounts receivable, etc.

Personal finance management as a freelancer

Freelancers may start their journey 100% motivated, but sometimes, clients don’t pay on time and work is not ensured every month. This can lead to a fluctuation in income and so, as mentioned above, it’s crucial that you understand how to create a good financial plan for freelancers.

Here are a few tips that you can follow to manage your finances as a freelancer:

#1 Track your expenses

It’s important to understand where your money is going – both personally and professionally. Your freelance business needs to cover your personal and professional costs, so keep a tab on what those are.

Review your expenses from the last 3 – 6 months and note all the fixed costs that you have: rent, utility bills, debt payments, hairdressers, annual renewals, etc. Also make a note of all other expenses (like annual renewals) – this will help you eliminate any wasteful spending habits and maintain control of your finances.

If you keep track of your freelance expenses, you won’t miss out on maximising your tax-deductible business expenses. This will help you reduce your tax bill.

What self-employed expenses can I claim? Tax deductions list:

- Transportation

- Travel expenses

- Health checks and eye tests

- Business insurance

- Accommodation

- Bank charges

- Childcare

- Using your home as an office

- Phone bills

- Annual staff party expenses

- Equipment expenses

- Professional development expenses

#2 Track your income (+ predict it)

Keeping track of every dollar that comes in through your income will help you understand where it’s going and how. Remember, your income is one of the main reasons why you’re a freelancer in the first place.

You need to understand exactly how much money you’re bringing in and how much your time is worth. You could also go one step further and ‘predict’ your income. This way, you’ll have a general idea of how much you need to be making in the next month.

For example, you could use a simple spreadsheet to track your freelance income. Record how much work you have already booked each month, what the project is about, the client and payment details (invoiced vs. paid).

#3 Separate business and personal accounts

To maintain a clearer picture of your business’s cash flow, it is crucial for you to have a separate business and personal account.

Keeping separate accounts will make accounting a lot easier and can also reduce your tax burden. It can also help you during audits from the tax office and prove to them that everything is well recorded.

Remember, your business income is not your personal income which is why it’s important for you to pay yourself a salary too.

#4 Consider your taxes

Running a business on your own means that you need to pay your own taxes.

In the case of freelance business owners, you are responsible for paying your taxes at the end of the year. Which means, you’ll have to put aside money for it on a regular basis.

How much tax should a self-employed person put aside?

It depends primarily on where you reside and the taxation scheme.

For example, in the US alone, income tax rates apply differently at different federal, state and regional levels. Once tallied with the self-employment tax, different freelancers get different percentages that they need to set aside.

Freelancers in Spain who work with national clients must include the IRPF (personal income tax) directly on their invoices. But when working with international clients, they will instead need to pay 20% of their pay to the Hacienda (tax agency) directly as well as fill out form 130 – an income tax form that should be submitted quarterly.

💡 Saving 10% – 30% of your monthly income for taxes could be a good starting point. However, the best way to know exactly how much you should put aside each month is to consult with an accountant in your jurisdiction.

Remember, everyone’s situation is different so the best thing to do is to plan for the worst-case scenario.

If you’re a digital nomad, you may even have to file tax returns in more than one country, depending on where you’re based and who you work with. It’s therefore important to understand your tax residency status in order to avoid any problems.

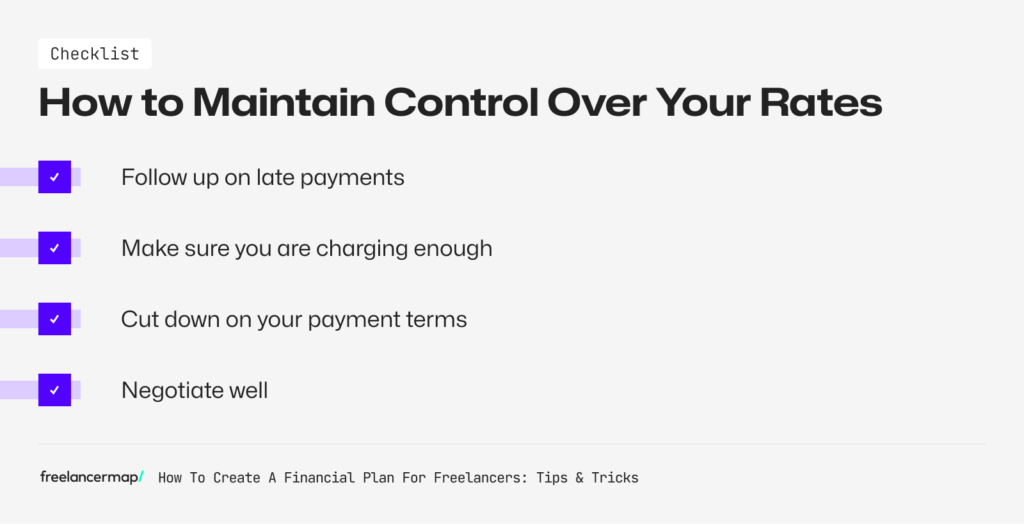

#5 Stay in control of your rates, terms and customer invoicing

Pricing, invoicing, agreements and contract terms are some of the not-so-fun tasks for freelancers. However, these things can affect both your freelance profits and financial plan and so you need to stay on top of them.

Freelancers face many challenges in the financial area:

- Late payments

- Low payments / underpayment

- Long payment terms (NET 30 / NET 90)

- Client negotiations (rates, contracts, etc.)

Follow up on late payments

In addition to inconsistent income and projects, freelancers have to often deal with getting paid late. In fact, according to freelancermap 2025 study, 25% of freelancers state that late payments are one of the biggest challenges they face.

Oftentimes, freelancers send out payment reminders that are due in weeks or months, and then as time passes, they forget about them, only to remember too late. But you’re providing a business for your clients and you deserve to get paid for it, on time.

Take some time every week to check-in with any outstanding payments or upcoming ones. Keep a note of all clients that have paid or have to pay you that week. You may also consider adding in a late fee to encourage your clients to pay on time.

Make sure you’re charging enough

Freelancers often undervalue their work and end up with low rates – especially at the beginning of their career. Make sure you charge your clients enough to reach your monthly income goal.

Remember, you are responsible for paying your own taxes and insurance and so your rates need to take that into consideration. Plus the hours you’re not working usually goes into the development of your business which also needs to be considered.

Cut down on your payment terms

Surprisingly, many clients and industries still think NET 60 or NET 30 is a fair payment term for freelancers. This means getting paid within 60 or 30 days of invoicing (plus the potential delays that might occur). Well, this won’t work for most freelancers.

Make it clear from the outset that you expect payment within 7 or 14 maximum days. You could consider 30 days for established clients or larger projects but it shouldn’t be the norm.

Client negotiations

It’s not only the length of your payment terms what you will have to negotiate with your client. It’s also potential late fees, rush fees, payment methods, the option to work with a freelance retainer agreement, etc.

Client communication skills are key to feeling confident when negotiating all the terms with the client. Do not forget your value and all that you will do for the client. It should be worthwhile for them as well as for you!

Use money management apps to automate your processes

There are lots of useful money management and accounting apps that can help you automate your financial reporting, invoicing and accounting. As a freelancer, you have limited time and resources, so try to leverage the power of these tools so that you may have more flexibility.

Of course, you can create invoices on Google Docs, but there are programs like Bonsai or Freshbooks, that allow you to send out invoices and make it easy for your clients to pay you.

For example, Bonsai is an all-in-one tool built for freelancers and not only does it allow you to track time and send invoices, but you can also use it to send out proposals and contracts, track your expenses, or send automated payment reminders. We highly recommend it and they offer a 7-day free trial.

Freshbooks is another app that you can use to track your expenses and automate your invoicing. It allows you to track your payments and makes it simple to create financial reports. You can try it for free for 30 days and then pricing plans start at $15.

Have a budget

This may seem like an obvious tip but it’s also an important one. A good financial plan for freelancers takes into account budgeting. Budgeting allows you to plan accordingly and not overspend during higher income phases. Some freelancers just go with the flow when things are looking good and don’t think about how much they have and how that relates to their spending.

Burying your head in the sand is an extremely bad idea when your finances are concerned. A creative job and free spirit aside, as a freelancer and your own CEO you have to take full responsibility when it comes down to managing the budget.

Know how much you spend and earn on a monthly and yearly average. If these averages don’t pan out, you know you have to start cutting your expenses.

You could consider using the 50/30/20 budget rule. This is where you first begin by figuring out all your necessary fixed costs. You then account it for 50% of your income while allotting 20% of it towards saving (retirement, investments, etc.) and 30% for spending on things you want (entertainment, vacations, etc.).

Also, it’s good practice to regularly review and modify your budget on an ongoing basis to ensure it works best for you and your business.

What are some tips you can follow for better budgeting as a freelancer?

- Monitor your finances regularly

Checking in with your finances is crucial. It will help you create a clearer picture of how effective your financial plan for freelancers really is. You could make this process as simple as signing in to your bank account every once in a while or checking to see if your revenue and income projections are on track.

Consider putting aside 15-20 minutes everyday to accounting. It will help you get ahead of any impending tasks and make financing a lot easier.

💡 Check out this video from Robert Vlach – a senior business consultant – which can give you in-depth understanding of financial self-management.

He also provides a free template that you can use to create a Personal Financial Plan For Freelancers

- Diversify your income sources

According to our survey for this year, 58% of freelancers work with multiple clients at any given time.

Aiming for several clients is a general thumb rule that any freelancer should follow. It might be a bad idea to get most of your income from just one main source. Why? Because it binds you to that particular client, making it harder to refuse requests, negotiate or just back out if you’re no longer happy with the business relationship.

Furthermore, if that one client suddenly runs into financial problems of their own or just decides to stop working with you, you might be in big trouble. That’s why you should always try to have at least a couple of different fairly equal income sources which balance themselves out.

- Plan for dry spells

Freelancing is, by nature, unpredictable. Some months, you may have more work than you can manage and other times, you may struggle to find clients. Your income is therefore bound to be inconsistent and can fluctuate month-to-month. Your financial plan for freelancers needs to take this into account.

It is crucial for you to save enough money to support yourself through any dry spells without work. Consider having a savings account that is specifically for emergencies only or an investing account. Ideally, you’ll want to save at least six months’ worth of expenses.

While not all freelancers start with a financial buffer (aka runway or financial cushion), every freelancer should strive to build one as the time goes.

Our freelancers recommend having at least €24,900 before taking the leap (Source: Freelancer Study 2025 – freelancermap).

You can choose to automate your savings so that you can send a percentage of your income into a designated savings account each month. The exact percentage depends on a number of factors like location and income but anywhere between 10-15% is a good idea.

How do you pay yourself a salary with an irregular income?

To understand how much you can pay yourself, you will need to calculate your net income. This is the money you actually own after expenses and operating costs.

The best way to stick to a consistent salary is to budget according to your lowest-paying month. That way, if you have more money during your busiest months, you can even it out over the year or even put it into investments and savings.

Remember, the key here is to be flexible and to stay on top of your expenses and your income.

#6 Plan for the future: Retirement & eventualities

This is another important tip when creating a financial plan for freelancers. Saving for retirement is crucial when working as a freelancer. Remember, the sooner you begin saving, the more time your money has to grow.

Setting goals, having an emergency fund, creating a good investment plan – these are all things you can do to plan for your future self.

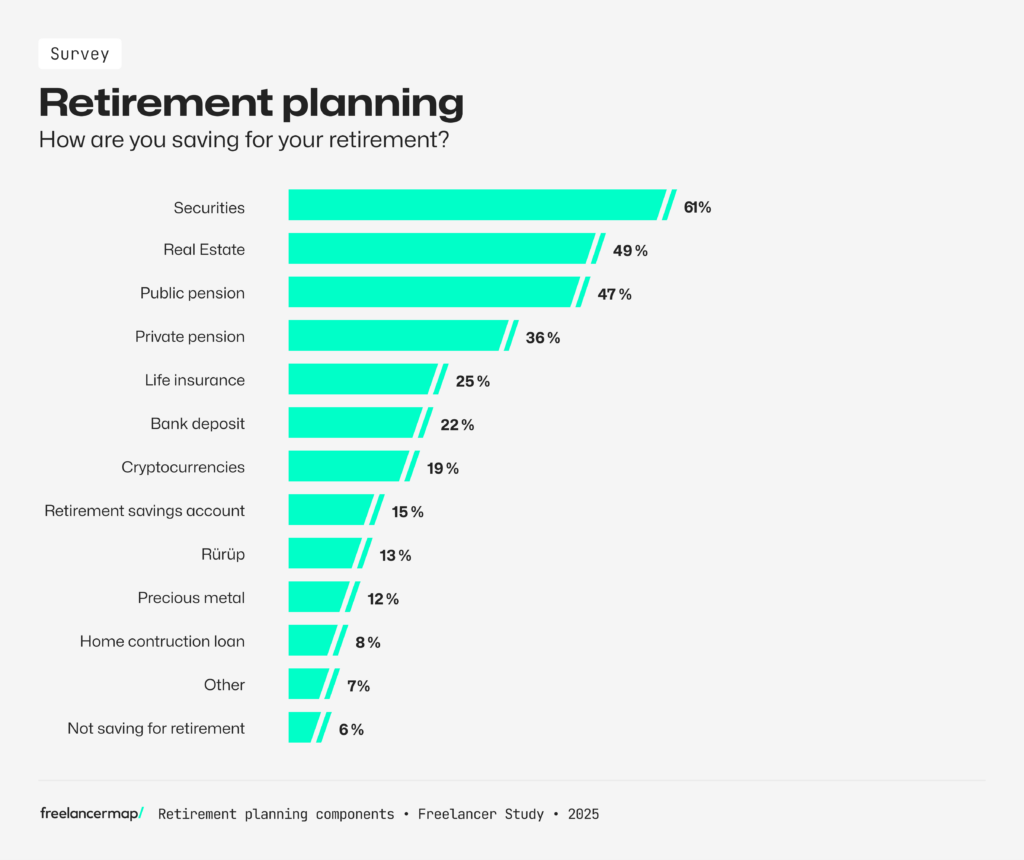

According to our survey 2025, the majority of freelancers (61%) save money for their retirement through securities such as shares, ETFs, funds, etc. What’s more, the average amount of money that they put aside each month is roughly around €1,098.

You could also consider signing up for any pension plans that may be available in your country. These could be either private- or government-sponsored schemes which will help you maximise your savings for the future.

1. Start investing

Having excess money as a freelancer gives you the opportunity to invest it. Smart investments mean more money, and more money means room for growth.

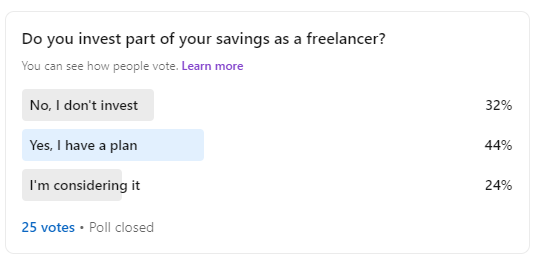

After running a short poll on LinkedIn, we found that only 44% of freelancers have a plan when it comes to investing their savings whereas 32% don’t invest at all. One of the reasons for this could be a lack of time and knowledge.

So where do you begin investing your savings? Smart investments!

The most important thing that you can do for your business is to invest in things that allow it to grow over time. Instead of just keeping all your excess cash in the bank, you can put some of it into investments in order to generate additional revenue. This is known as corporate investing.

Remember, money loses its value over time so any delay in investment is a lost opportunity. All businesses make investments to grow and so freelancers must too.

Here’s how you can get started with corporate investing:

Learn the basics

You’ll want to begin by first learning the ins and outs of investments. Make sure you spend enough time understanding the basics of investing and the principles behind what you want to invest in. Luckily, there are tons of websites and blogs dedicated to investment for you to learn just about anything, including different types of investments and common terminologies.

Understand your risk profile

Also, keep in mind that one of the most important things to consider when investing is the level of risk that you are willing to take. Every freelancer is different and is therefore willing to take different levels of risk when it comes to investing their money.

Understanding your risk profile can help you make informed decisions and invest in the right stocks that align with your goals.

There are usually 3 main risk profiles that you can have:

- Conservative: If you’re a beginner, it’s usually a good idea to have a conservative risk profile. The options we mentioned above (stocks, crypto, bonds) are low-risk investments that prioritise stable returns over higher ones.

- Moderate: Investors with moderate risk profiles tend to take some risks while balancing low- and high-risk securities such as equity mutual funds and real estate.

- Aggressive: These investors prioritise growth and follow an investment plan that involves aiming to maximise financial gains by taking high risks..

It’s crucial for you to identify your risk profile in order to make sound investment decisions that align with your financial goals and risk tolerance. Ultimately, your investment strategy should balance what you’re comfortable with contributing as well as what you’re willing to accept in return.

Invest in what you can afford

Next, you’ll want to invest what you can afford. That means staying away from complex high-fee investments like mutual funds and toxic investment schemes that promise ‘high-yields’.

Consider low-risk investments, especially if you have a conservative or moderate risk profile.

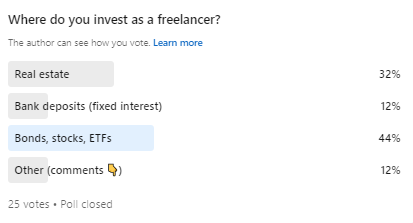

44% of freelancers from a short survey conducted on LinkedIn state that they invest their savings in federal bonds, stocks, or ETFs. Also, real estate is a beloved investment for freelancers (32%).

Keep your debts in check

If you have any lingering debt, it’s very important that you pay it off first before making any investments. When possible, consider paying off more than your minimum payments – tackling it first will help you save hundreds or thousands in interest.

Also consider limiting your use of credit cards and other credit products. These high-interest credit card debt costs more over time making it much more difficult to pay off.

💡 Sometimes corporate investments can help you reduce your tax obligations. However, these will look very different depending on the size of your business and where you’re located.

Get yourself covered with good insurance

Investing in the right insurance as a freelancer is crucial for protecting yourself and your business from unforeseen expenses and potential lawsuits. Having good insurance coverage can help you avoid financial strain in situations like a broken laptop during a business trip or accidentally damaging someone’s property while working.

We recommend checking SafetyWing’s Remote Health Insurance (click to get access to unique plans exclusive to the Freelancermap community).

By investing in the right insurance coverage, you can have peace of mind knowing that you are financially protected in case of any unexpected events or accidents that may occur during the course of your freelancing career.

Other investments in your freelance business

A good financial plan is not only about making your money grow. As a freelancer, you will also need to invest in yourself and your business. How?

Improve your skills with courses and workshops. You can increase your niche knowledge and get really good at one specific thing. Or you can diversify your skillset and aim for things that synergize well with your business.

Also attending conferences is a great idea as this willl give you a chance to expand your network, learn from fellow freelancers and get inspiration for your own business.

Another great way to invest your money is to expand your business. Freelancing doesn’t have to be a one-person show. Getting a lot of clients and often having to decline good project offers is a sign that you want to hire additional people.

Collaborating with other freelancers is a great option to take on big challenging projects, which were probably out of your scope before.

#7 Get professional help with a financial advisor

The best investor and finance tip that you can get is to speak to a financial advisor. Not only will they help you create a personalised investment plan, they can give you the freedom to not worry about your finances and instead focus on growing your business.

They can also really help you understand your retirement plan and coach you through any volatile situations. Plus, if you’re corporate investing, they can walk you through any general or complicated tax procedures.

Accountants can also be very helpful in your business. They can help you understand how the tax system works so that you can do everything by the book and take advantage of tax breaks.

Conclusion

Mastering a financial plan for freelancers is key to building a successful business. Tracking your income, making note of your expenses, planning for retirement, investing – these are all things that you can start today to improve your finances.

It may take some time and focus but it can help you achieve both your financial and personal goals.

Please note that we’re not registered accountants or tax professionals, so please take these tips for what they are. If you need further help, please get in touch with a professional so that you can go through your particular case with them.