Being a freelancer may come with a lot of perks, but unfortunately, an automatic workplace pension isn’t one of them. While employees at a company can sign up for their company’s pension scheme, freelancers are in charge of arranging their own pension and putting aside money to contribute towards their future.

- Do freelancers receive a pension?

- Freelancer pension: which one is right for me?

- How do freelancers prepare their retirement plan?

- Tips to Prepare for Retirement as a Freelancer

- How do I choose the right freelancer pension?

- Tips on how to save for retirement

Do freelancers receive a pension?

The short answer is yes, freelancers are eligible to receive a pension, depending mostly on the country in which they reside. For example in countries like the UK, freelancers are entitled to the state pension if they have made several national insurance (NI) contributions over the years.

Join our freelancer community today!

Create your profile in just 2 minutes and start attracting new clients.

Likewise, in the US, self-employed individuals are eligible to open and contribute to a SEP IRA (Simplified Employee Pension IRA).

There are also private pension options available for freelancers who are looking to have money on top of their state pension.

Freelancer pension: which one is right for me?

As stated above, there are options available for freelancers looking to secure a pension. These can be seen as follows:

State pension

Depending on where you work, you are entitled to a public/state pension as a freelancer.

In the UK, the state pension is part of the government’s pension arrangements and is a weekly payment that you receive when you reach state pension age. The maximum state pension is £203.85 per week (tax year 2023/24), however, the actual amount depends on your National Insurance (NI) record. It is usually paid every 4 weeks into an account of your choice.

💡 Keep in mind that the state pension is unlikely to be enough for you to live comfortably on. It is therefore advisable for you to obtain an additional private pension or another financial secure alternative.

Similarly, in Spain, self-employed individuals can now benefit from a state pension as a result of the government’s recent changes to the contributions system. Workers will be allowed a pension of €377.92 more per month, if they contribute €144.49 more to Spain’s social security system.

The threshold for this is a monthly earning of €1,416.60 a month, which is 1.5X the current minimum contribution base. According to new rules, the new way of calculating contributions will be based on net earnings, so some will pay less but most will contribute more.

In Portugal, freelancers can benefit from contributions if they register with the Tax department, which will in turn inform Social Security. However, if you work for a company as a freelancer, the company in question will need to register with Social Security on your behalf and also pay your contributions.

If you’re a self-employed individual, you will need to make payments on a monthly basis. Your contribution will be calculated as per the following rules:

- 70% of the total charged for services rendered or

- 20% of income related to the production and sale of goods or

- 20% of the total charged for services rendered in the fields of hospitality, restaurants and drinks sectors.

If you’re a freelancer with a contract, the monthly contribution will be paid by your company and will be 34.75% of your gross salary. This number can be broken down into:

- 11% supported by you

- 23,75% supported by your employer/company

Because this payment is made directly to the Social Security by the company, your share of contribution will already have been discounted from your net salary.

In addition, those living on green receipts in Portugal can also benefit from a retirement pension once they turn 66 and 4 months and have contributed for at least 15 years to Social Security.

Private pension

Private pensions are a type of pension that you can set up on your own to help you save money for retirement. These types of pensions are the most popular with freelancers, mostly because of the number of options available to choose from.

Another reason is that these pensions have the ability to grow over time, thereby increasing your pension pot.

The best part about these systems is that they can be personalized to suit your needs. You can choose a private pension system in your country that is shaped in accordance with your standards and expectations.

Other types of freelancer pension plans

As mentioned above, the type of pension plan that you can sign up for depends primarily on where you live. In the US, for example, apart from government pension and personal pension, freelancers can also make use of Solo 401k plan or a defined benefit plan.

Likewise, if you reside in the UK, you can make use of a defined benefit plan or a defined contribution plan.

How do freelancers prepare their retirement plan?

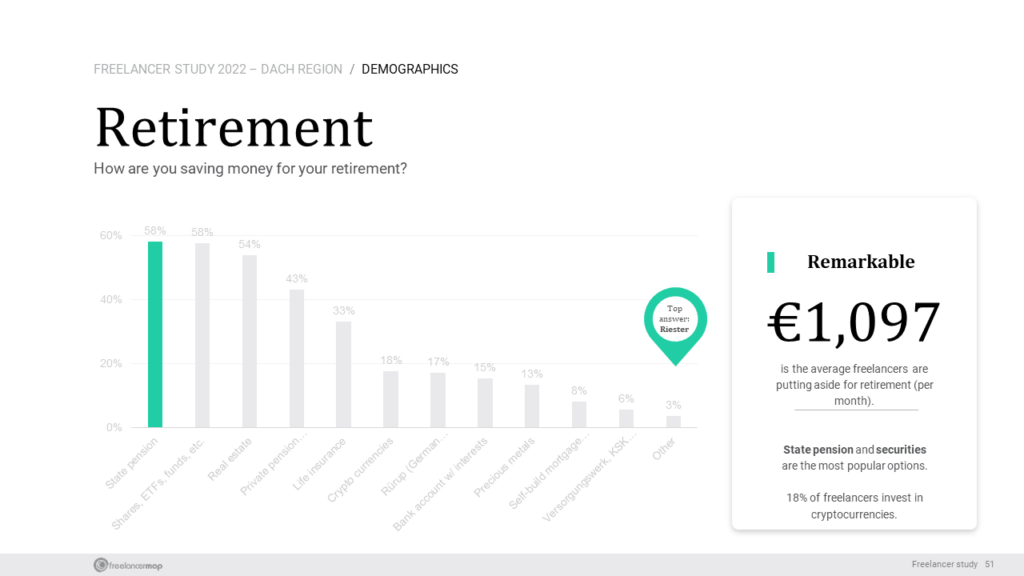

We ran a freelance survey last year asking freelancers about their plans for retirement and how much are they setting aside each month towards it.

Results show that the vast majority of freelancers in Germany (58%) are relying on state pensions as well as shares, EFTs, and funds for their retirement plan.

In addition, data suggest that freelancers set aside approximately €1,097 per month towards their retirement.

Information pulled from our LinkedIn polls also suggests that investing is a topic most freelancers have thought about.

44% of freelancers state that they have a plan for investing their savings whereas 32% state that they don’t have a plan. 24% of freelancers are considering investing part of their savings, but haven’t started yet.

Tips to Prepare for Retirement as a Freelancer

As you have read, every freelancer has a different plan. Where do you stand?

Are you really budgeting for retirement? Have you made the time to work out what you’ll really need, and how you’re going to get there?

Chances are, you haven’t. But don’t worry!

Stephen Erich shared with us six quick tips that can help you prepare for retirement without adding any extra burdens to your busy freelance schedule.

As a freelancer, you’ve probably set a goal to earn a certain amount each month. You know what your expenses are and you know what you need to be comfortable. You’ve probably even budgeted extra in case of emergencies. Chances are, though, your monthly income goal isn’t taking your retirement into consideration.

1. Define Your Retirement

This is key. The main reason I initially delayed preparing for retirement is that I didn’t want the stereotypical ideal of a mansion and a yacht, so I figured I didn’t need to worry about it. I didn’t realize that retirement, fundamentally, is just financial freedom, and that it could take on whatever form I wanted to give it.

So what do you want your retirement to look like? Do you want a country home or a condo in the city? A tiny house or land in a foreign country? Do you want to be able to vacation, or volunteer, or even continue working, but at a relaxed pace? Do want it to last 10 years or 40 years?

You can do anything, as long as you identify it first.

Once you have a vision, you can easily work out what your monthly and annual expenses will probably be. Remember to consider additional health-related expenses. Multiply your expenses by the number of years you expect to need it, and you’ll know exactly how much your retirement goal is, how much time you have to achieve it, and why.

2. Identify Your Strengths

Once your retirement goal is clear, take a look at your skills and your current income. Is your income high or low? Is it tied to the number of hours you work or the amount of value you create? Is it temporary or perpetual?

By answering these questions, you can figure out whether you’re best off investing your current income into retirement funds, or devoting your time to developing value that generates passive income.

In other words, if you earn a high wage, but it’s tied to the number of hours you bill your clients (eg. lawyers, consultants), you should consider investing everything you can now, so that when you stop working and your income dries up, you can live off of today’s excess.

If, on the other hand, you’re current income is tight, but you have a talent or resource that you can leverage to create long-lasting value (eg. writing a book, starting a website, owning real estate), you should consider ways of building that passive income to a sustainable point.

For many, there can be some balance between these two. And remember that even though you may not have a lot of discretionary funds right now, technology keeps on making great investment opportunities easier for normal people.

3. Develop an Exit Plan

While you may not have the benefit of an employer contributing to your 401k as a freelancer, you have the benefit of owning equity in your business. The client relationships you’ve developed, the goodwill associated with your branding, and any equipment you may have accumulated over the years are all worth something, and instead of abandoning all this value when you stop working, consider selling your business, or parts of it.

This might mean you need to incorporate if you haven’t already (which would then also enable you to contribute to your 401k as an employer as well as an employee), but not necessarily.

4. Pay Your Taxes

Depending on the country you’re from, your social security is likely based off of your most profitable tax years. Reporting your full income now allows you to receive your maximum social security payout during your retirement years. This is not only ethical, but good for your retirement, too.

5. Clear Your High-Interest Debt

When deciding whether to invest or pay off debt, take a look at your interest rates. For high-interest debt like credit cards, it’s always better to pay those off before devoting cash to investing. The 20% interest payments you’ll be forced to make will more than cancel out your 5-10% return on an investment during that period.

Mortgage or student loan debt are probably the two kinds of debt that you don’t need to pay off before you start investing, since those interest rates should be less than what a good investment will give you. But again, it all depends on the rates.

6. Automate Your Retirement Contributions

Once you know what you want out of retirement and have a basic idea of how you’re going to get there, it’s time to actually find an investment manager that will allow you to set recurring deposits so that you can let them do the investing, while you focus on your work. Services like Wealthfront or Betterment really make it easy with simple and professional robo-advisor services.

Once you’ve decided which service is best for you, it’s as simple as scheduling recurring deposits every month (or for best results, as often as you get paid) for the amount that you’ve already determined you’ll need in order to meet your retirement goal. Many services will even help you figure out what that amount is!

If, like most freelancers, you are paid whenever you complete a project, you may not have a single date that works best for scheduling. You can get around this by using features like Betterment’s SmartDeposit, which automatically makes a deposit whenever your bank account goes over a certain threshold that you decide. That way, every time you get paid, the excess is automatically invested.

In conclusion, remember the importance of having a vision.

Your retirement plan is one of the easiest things to set and forget, as long as you take the time at the beginning to set it right. So knock it out now, and get back to work knowing that you’re making the most of your time.

How do I choose the right freelancer pension?

Choosing a pension plan that’s right for you involves comparing the details of different plans available to you. Here are a few things you should consider when doing so:

#1 Contribution limits

Before choosing a plan, make sure you look into the maximum and minimum level of contributions allowed.

Since freelancers often have irregular income, you’ll want to check if you have to make regular payments or if you can vary how much and when you pay.

#2 Fees

This is perhaps the most important factor to consider when choosing a pension plan. Some plans have annual fees that cover the cost of running and administering your pension scheme whereas others can include additional fees such as administration fees, transfer charges, charges for managing your investments, penalties, etc.

#3 Investments

When choosing a plan, you will want to check whether there is clear information about where you can invest your contributions and how.

Make sure you are happy with the level of risk you are taking and also that the scheme offers the right range of investments for you.

#4 Management

Lastly, you will want to choose a plan that offers help and support and allows you to monitor your investment options. For example, is there an online account? Can you check your balance and make contributions online?

Tips on how to save for retirement

One of the most important things you can do for your future is start thinking about your retirement plan and saving for retirement as soon as you can. This is because the sooner you begin saving, the more time your money has to grow.

Not sure how to start saving as a freelancer? Check out these tips:

#1 Set goals

The first step and perhaps most important step to saving for retirement is setting goals. By creating a clear action plan, you will be able to decide how much you need to start saving. When creating goals, take into account your lifestyle, timeline and retirement savings plan.

Also remember to track and review your goals. This will help you stay focused and let you know if you are still on the right path.

#2 Spend less

This may seem like an obvious tip but you’ll be surprised to learn just how many people don’t follow this rule. Spending less money than you make allows you to invest your money for long-term growth and can also eliminate any debt that you may have.

Begin by creating a realistic monthly budget. This will help you prioritize your spending and help you keep track of the money that’s going in and out of your bank account.

#3 Have an emergency fund

Having an emergency fund is almost as important as saving up for retirement. This is mainly because freelancing can be inconsistent when it comes to making money and if you’re having trouble finding clients, your business will suffer.

For this reason, consider setting aside money every month to go towards your emergency fund.

#4 Start an investment plan

Having an investment plan in place can help you allocate some of your monthly funds (not from your emergency pile!) towards ventures that can over time act as an alternate source of income and safety net.

Consider consistently investing small amounts of money out of your earnings every month. 10-20% of your income is a good place to start.

#5 Diversify your portfolio

As you save for your retirement, be sure to spread your savings or investments across several platforms and mediums. Diversification will help you reduce the amount of risk you’re exposed to in case of a bad event and may actually improve your potential return.

#6 Contact an investment professional

Knowing when and how to retire can sometimes be hard to determine, especially if you work as a freelancer. If you find yourself getting overwhelmed, perhaps it’s time to contact a professional.

Get in touch with other freelancers or ask your friends for recommendations on who they use. A good advisor will set up a retirement plan that fits your budget and lifestyle and will minimise your stress by taking the burden off of your shoulders.

How are you planning for retirement? Let us know in the comments down below!

Natalia

Puedes comentarme, que es más beneficioso para una persona como yo que tengo 59 años, donde puede hacer aportes a pensión y si es benéfico o no, para mi.