Self-employment (also called bogus self-employment) is often hailed as a pathway to independence, allowing individuals to be their own bosses and manage their work schedules. However, not all self-employment is created equal. False self-employment, a scenario where individuals are classified as self-employed but work under conditions akin to regular employment, is a growing concern in Europe. This article delves into the concept of this issue, its implications, and how different European countries are addressing the issue.

- What is false self-employment?

- False self-employment – A Europe-wide phenomenon

- Checklist for identifying false self-employment

- Country-specific designations and approaches

- Tips to avoiding false self-employment

- Examples of false self-employment

- Conclusion

What is false self-employment?

False self-employment occurs when a worker:

- is labelled as self-employed but is, in reality, dependent on a single client

- lacks entrepreneurial freedom

- is integrated into the client’s work organisation.

This misclassification can have severe implications for both workers and employers, leading to loss of social security benefits for workers and legal and financial risks for employers. Economically, it distorts labour market statistics and undermines the social security systems designed to protect workers.

According to a report published by the European Platform in 2020, approximately 4.3% of jobs in Europe are categorised as bogus self-employment.

Addressing this issue requires a multifaceted approach. Governments must implement effective policies and collaborate internationally to set standards. Businesses should ensure compliance with labour laws and promote genuine self-employment.

Supporting workers through legal assistance, training, and education programs is also essential. Best practices include transparent hiring practices, regular audits, and fostering an environment that values fair labour practices.

Join our freelancer community today!

Create your profile in just 2 minutes and start attracting new clients.

False self-employment – A Europe-wide phenomenon

The issue of false self-employment is prevalent in many European countries and is increasingly being addressed by authorities and legislators. Although the exact definitions and legal frameworks vary, there are some commonalities:

- Dependence on a single main client

- Lack of entrepreneurial freedom

- Subjection to instructions

- Integration into the client’s work organisation

According to our latest Freelancer Study 2024, 37% of freelancers perceive false self-employment as a challenge.

This issue has dire consequences for workers, who miss out on social security benefits, face job insecurity, and experience financial instability.

For businesses, misclassification can lead to legal risks, financial penalties, and damage to their reputation. Broadly, this bogus self-employment undermines the labour market and social security systems, affecting economic stability and social welfare.

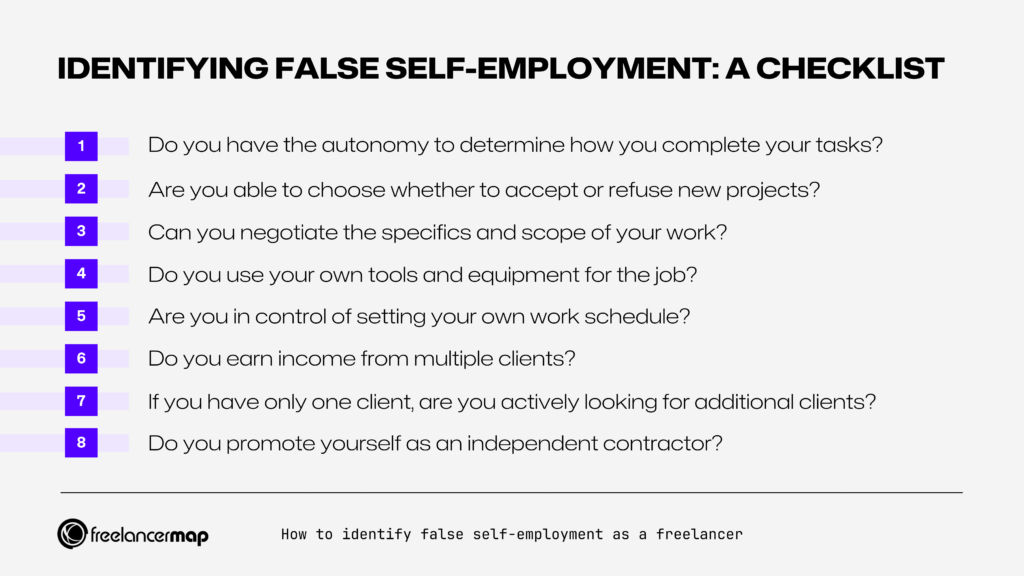

Checklist for identifying false self-employment

False self-employment can quickly become a significant issue. Therefore, it is wise to understand the criteria from the outset and regularly evaluate your situation to ensure you are not mistakenly classified as self-employed. The following checklist can assist you in this assessment.

- Do you have the autonomy to determine how you complete your tasks?

- Are you able to choose whether to accept or refuse new assignments or projects?

- Can you negotiate the specifics and scope of your work?

- Do you use your own tools and equipment for the job?

- Are you in control of setting your own work schedule?

- Do you earn income from multiple clients? (Ensure that no single client accounts for more than 80% of your total income)

- If you have only one client, are you actively looking for additional clients?

- Do you promote yourself as an independent contractor or self-employed professional?

Country-specific designations and approaches

Different countries have different definitions and criteria for when it comes to dealing with false self-employment. Let’s take a look at how some European countries define the term and what penalties and measures they take to tackle it:

False self-employment in Germany

In Germany, false self-employment, or “Scheinselbstständigkeit,” is scrutinised by the pension insurance authority, which uses various the following criteria to determine if genuine self-employment exists:

- The lack of decision-making autonomy

- Dependency on the client for more than 83% of their income

- Integration into the client’s operations

- Work equipment is provided by the client

- Working at the offices of the client

Recent cases have highlighted the challenges in distinguishing between true self-employment and disguised employment, with significant legal and financial consequences for those found non-compliant.

Investigations into “Scheinselbstständigkeit” are usually carried out by the German Pension Insurance Association but can also be done by the labour court, social or health insurance companies, or the tax office.

Risks and penalties for false self-employment in Germany

For clients, they may have to pay the freelancer’s social security fees as well as income tax – a consequence that can have a dire impact on the company’s cash flow. In addition, they might even be hit with a tax evasion suit.

Freelancers, on the other hand, could risk losing their freelance status and might have to make back payments to the German national pension system (“Deutsche Rentenversicherung”).

📖 Want to start as a freelancer in Germany? Read more in our post “Freelancing in Germany: Guide & Insights“

False self-employment in UK

In the UK, false self-employment is also referred to as disguised employment or misclassification of an independent worker.

The UK’s IR35 legislation aims to tackle disguised employment by determining the status of workers. The IR35 test assesses whether a contractor would be considered an employee if the intermediary (often a limited company) was not used. Some of the criteria that indicates if a worker is misclassified as self-employed in the UK includes:

- No right to substitute yourself with another worker

- Inability to set own work hours

- Reliance on a single client for financial provision

- Integration into employee’s organisation

- No personal entrepreneurial action

- Work equipment provided by employee

This legislation is particularly relevant in the gig economy, where many workers operate through intermediaries. The enforcement of IR35 has led to notable cases where companies and contractors faced hefty fines for non-compliance.

Risks and penalties for false self-employment in UK

In addition to hefty fines, employees in the UK are subject to income taxes and National Insurance payments through the PAYE (Pay as you earn) scheme, which employers are required to pay on behalf of their employees.

Freelancers and independent contractors are also subject to these taxes and are required to fulfill them annually. If found guilty, both the employee and the contractor may be sued for tax avoidance or tax fraud.

📖 How To: Going Freelance In The UK → Read the full guide

False self-employment in Belgium

Belgium uses the term “schijnzelfstandigheid” to describe false self-employment. The Belgian government has established clear guidelines to differentiate between employees and self-employed individuals, including these factors:

- No worker’s participation in the company’s profits or losses

- No proper capital investments in the company

- No responsibility or decision‑taking power in the company

- The certainty of getting a regular payment

- The fact of having just a single and unique customer company

- The fact of having no personal workers/the fact of not being an employer

- The fact of not being able to organise one’s working period

- The existence of in-house control procedures, with related sanctions

- No decision‑taking power concerning customers’ invoicing

Risks and penalties for false self-employment in Belgium

If you are deemed to be falsely self-employed, your client will incur a significant penalty. Reclassifying a freelancer as an employee imposes an additional burden on the company, requiring compliance with social security payments (such as holiday allowance, indexation, etc.).

In an employment situation, the employer is responsible for paying social security contributions from both the company and the employee sides. If reclassification occurs, the company may be required to pay 3-7 years’ worth of these contributions.

This situation can also lead to potential disputes over tax payments and VAT charges, as well as additional fines that the company may be liable for.

False self-employment in France

In France, false self-employment, or “faux travail indépendant,” is subject to stringent controls and high penalties for violations of labour laws. The criteria for identification in the country includes:

- Working conditions (hours worked and place of work)

- Whether work is directed by employee or by the freelancer

- Ownership of equipment used for work

- Economic dependance

- Failure to declare employees (for the company)

The French labour authorities conduct thorough inspections to ensure compliance with labour laws.

Risks and penalties for false self-employment in France

Violations can result in significant fines and legal repercussions, including criminal convictions and imprisonment for the employer. Self-employed individuals, on the other hand, may be subject to sanctions by social institutions if proved that they accepted the work knowingly.

The rigorous approach aims to protect workers’ rights and ensure fair competition among businesses.

False self-employment in the Netherlands

The Netherlands addresses false self-employment (Schijnzelfstandigheid) through the DBA Law (Wet Deregulering Beoordeling Arbeidsrelaties), which governs the assessment of labour relationships. The DBA Law provides clear criteria to distinguish between genuine self-employment and disguised employment. This criteria includes:

- If a client determines how you complete a project

- Inability to substitute yourself with another worker

- Fixed salary per month, even on sick days and days off

The law’s implementation includes regular audits and inspections to enforce compliance, with recent cases underscoring its impact.

Risks and penalties for false self-employment in the Netherlands

If the Tax administration in the Netherlands (Belastingdienst) determines that false self-employment has occurred, employers may receive a fine and will need to pay social security premiums. The self-employed individual will most likely lose any right to tax benefits.

False self-employment in Italy

In Italy, “falso lavoro autonomo” refers to false self-employment, which various laws aim to combat.

The Italian government has introduced several measures to promote genuine self-employment and prevent misclassification. These include incentives for businesses to hire workers on standard employment contracts and penalties for those found to be falsely self-employed.

The criteria for identifying false self-employment in Italy is if at least two of the three conditions are met:

- Working with the same client for more than 8 months per year for 2 consecutive years

- Income from a client represents 80% of the worker’s finances for 2 consecutive years

- Presence of workspace for the worker at client’s company

Risks and penalties for false self-employment in Italy

Clients who are charged with false self-employment have to pay past contributions and salaries for the worker. They may also be hit with hefty fines and can even face imprisonment.

If the worker is found guilty of having knowledge of being falsely self-employed, they may also face prosecution.

False self-employment in Spain

In Spain, false self-employment is referred to as “Falso autónomo”. It describes workers who are classified as self-employed but work under conditions similar to employees. The criteria for being classified as falsely self-employed in Spain are as follows:

- Consistent salary month after month from the same client over an extended period of time

- Supervision by the employer when carrying out a project

- Regularly attend work in accordance with a timeline

- Using employer’s work materials

Spain has implemented legal measures to address “falso autónomo”, particularly in the gig economy. Spanish authorities have introduced specific regulations and enforcement mechanisms to curb this practice, ensuring that workers receive appropriate protections and benefits.

A main example of the hiring of bogus freelancers has been in the field of digital delivery platforms. Because of this, the government of Spain was forced to establish a law called the “rider law”, which establishes the presumption that the employees of these platforms are salaried employees.

Risks and penalties for false self-employment in Spain

Misclassification of employees can lead to significant legal and tax implications. Depending on the seriousness of the infraction, the penalties that companies have to pay range from €3,126 – €10,000.

In addition to fines, the Labour Inspectorate may demand that the employer pay social security contributions. What’s more, if the combined defrauded social security contributions exceed €50,000, it may be considered a crime.

📖 Being self-employed in Spain: rates, taxes, visa requirements & tips to find clients

False self-employment in Sweden

Sweden has several laws that aim to protect workers from false self-employment, also known as “bogus self-employment”. If a self-employed individual meets the following conditions of the personal law in Sweden or “arbetstagarbegreppet”, they are regarded as falsely self-employed:

- The employee and the worker have an employment contract

- The worker is obligated to perform work personally i.e. they are not allowed to substitute another worker

- Equipment is provided by the employee

- Not allowed to perform similar work for other clients

- Employer states working conditions and work hours

- Employer provides worker with equipment needed to perform work

- Contract between parties is long-term

- Worker has same status as a regular employee

False self-employment is an old phenomenon in Sweden used in times of recessions, as stated by economist Annette Thörnquistand. It has been recently linked to labour migration and social dumping and is often associated with exploitation and survival strategy.

The criteria that defines employment in Sweden is regulated by the Swedish Employment Protection Act (LAS) but action is usually initiated by Swedish unions.

Risks and penalties for false self-employment in Sweden

A company found guilty of false self-employment must pay the salary and employment benefits for the damage incurred to the worker. The worker, on the other hand, will lose tax advantages and social benefits and may find it difficult to get more work in the future.

| Country | Term | Solution to false self-employment |

|---|---|---|

| Germany 🇩🇪 | Scheinselbstständigkeit | Regular audits done by the German Pension Insurance (Deutsche Rentenversicherung), tax offices, or custom authorities. |

| UK 🇬🇧 | Disguised employment | IR35 legislation assesses the employment status of workers through a test. |

| Belgium 🇧🇪 | Schijnzelfstandigheid | Establishment of clear guidelines to differentiate between employees and self-employed individuals. |

| France 🇫🇷 | Faux travail indépendant | Thorough inspections to ensure compliance with labour laws. |

| Netherlands 🇳🇱 | Schijnzelfstandigheid | Regular audits and inspections to enforce compliance. |

| Italy 🇮🇹 | Falso lavoro autonomo | Introduction of several measures to promote genuine self-employment and prevent misclassification. Incentives for businesses to hire workers on standard employment contracts. Introduction of penalties for those found to be falsely self-employed. |

| Spain 🇪🇸 | Falso autónomo | Implementation of legal measures to address false self-employment, particularly in the gig economy. Introduction of specific regulations and enforcement mechanisms. |

| Sweden 🇸🇪 | Bogus self-employment | Conducted several reports and examinations about employee working conditions. Used reports to inform politicians and policymakers. |

Tips to avoiding false self-employment

Avoiding false self-employment is crucial for both freelancers and clients to ensure legal compliance and for protecting their rights. Here are some tips to help you steer clear of false self-employment:

For freelancers

#1 Diversify your client base: Work for multiple clients rather than relying on a single client for most of your income.

#2 Maintain independence: Make sure you have control over how, when, and where you complete your work. Avoid situations where you are subject to the same rules and supervision as an employee.

#3 Use written contracts: Always have a written contract outlining the scope of work, payment terms, and project timelines. Ensure it clearly states that you are an independent contractor.

#4 Invest in your business: Have your own business infrastructure, such as a dedicated workspace, business cards, and a professional website. This helps demonstrate your status as a genuine business entity.

#5 Handle your own taxes: Manage your own taxes, insurance, and other business expenses. Do not let clients withhold taxes on your behalf.

#6 Set your rates: Determine and negotiate your own rates rather than accepting a salary-like payment structure.

#7 Promote your business: Actively market your services to attract new clients. Participate in networking events, online platforms, and professional communities.

#8 Avoid employee-like benefits: Decline any employee-like benefits offered by clients, such as paid leave, pension contributions, or health insurance.

For clients

#1 Draft clear contracts: Use clear, detailed contracts that outline the nature of the work and the independent contractor relationship.

#2 Avoid control and supervision: Allow freelancers to manage their own work schedules and methods. Avoid imposing strict work hours or closely supervising their activities.

#3 Distinguish from employees: Ensure freelancers are not integrated into your company’s organisational structure. They should not have job titles or perform work indistinguishable from your employees.

#4 Payment practices: Pay freelancers per project, milestone, or deliverable, rather than a regular salary. Avoid providing employee-like compensation or benefits.

#5 Communication: Maintain professional boundaries. Communicate through official channels and treat the relationship as a business-to-business engagement.

#6 Consult legal advice: Regularly review your freelancer agreements and practices with a legal advisor to ensure compliance with local labour laws and regulations.

#7 Monitor compliance: Stay informed about the legal requirements and any changes in labour laws that may impact the classification of workers.

By following these tips, both freelancers and clients can establish and maintain a clear and lawful independent contractor relationship, minimising the risk of false self-employment.

Examples of false self-employment

Example 1

A young development team hires a former employee who has just finished her parental leave. She wants to work a few hours a day for her old company while also working for other clients, so she prefers to work as a freelancer.

After a year, her workload increases and starts to resemble a full-time job; due to time constraints, she is no longer able to work for other clients. After a surge of projects, she takes a two-week vacation from her client. Upon returning from vacation, it is decided that she can use a PC in the office to facilitate her work.

This is a classic case of false self-employment. It developed over time and was not present from the beginning. The following points indicate false self-employment:

- Dependence on a single client

- Use of the client’s equipment

- Vacation entitlement

Example 2

A project manager’s company had to file for bankruptcy. After a long period of unemployment, a company offers him a position. The project manager is offered the opportunity to manage a young, dynamic team and their projects.

The freelancer does not work from home and coordinates projects online; instead, he works from the company’s office. There, he has access to company equipment, coffee, and other provisions; the package also includes access to the company’s gym.

Once again, there is personal dependence. The indicators are similar to those in the first example. The difference is that the false employment is evident from the beginning. Both parties should have realised that this is not independent work.

Conclusion

False self-employment is a pervasive issue across Europe, with significant implications for workers, businesses, and the economy.

Addressing this problem requires concerted efforts from policymakers, employers, and workers alike. By understanding the nuances of bogus self-employment and implementing robust measures to combat it, we can ensure a fairer and more equitable labour market.